Relationship Marketing For Finserv: How To Build Better Customer Relationships From Acquisition To Retention

- 0.5

- 1

- 1.25

- 1.5

- 1.75

- 2

Tim Glomb: Well, hello and welcome to our main event today. Today, I am Tim Glomb. I'm going to be your host. I'm the VP of content here at Cheetah Digital, and host of Thinking Caps, is why we always wear hats here. But today, we're going to discuss ideas around this finserv industry, but through the lens of what consumers expect, want, and need today, when you're looking at a customer life cycle there. To do this, we're going to be citing some most recent consumer trends and attitude stats that were published in mid- March of 2022 revealing how consumers want to be engaged across marketing channels: their propensity for mobile as a tool, as well as some of the good and bad when it comes to brand experience. Usability of products and services, as well as some ideas around privacy value exchange, what data consumers are willing to give up for your customer acquisition efforts, et cetera, et cetera. We'll also take a look at how Kiwibank created a textbook experience based on a value exchange with customers to gather the ever- important zero- party data to then offer personalized offers and content related to their services. It's a really, really good case study and a great example of a financial institution such as banks, credit card companies, insurance, et cetera, should be acting in the market. And last but certainly not least, my co- host today, Justin Orgel, is Cheetah Digital's senior director of global strategic services. He works with all of our great clients. He pulls off all kinds of magic for them, and he's going to share some insights into the great work we're doing with our finserv clients, which happens to be one of our largest pools of clients that we have here at Cheetah. He's going to discuss some things there. Justin, I appreciate you coming on. How you doing? You're in Miami today? Everything good?

Justin Orgel: I'm in Miami, yeah. Thanks. Tim. Great to be here. Happy to be here with you.

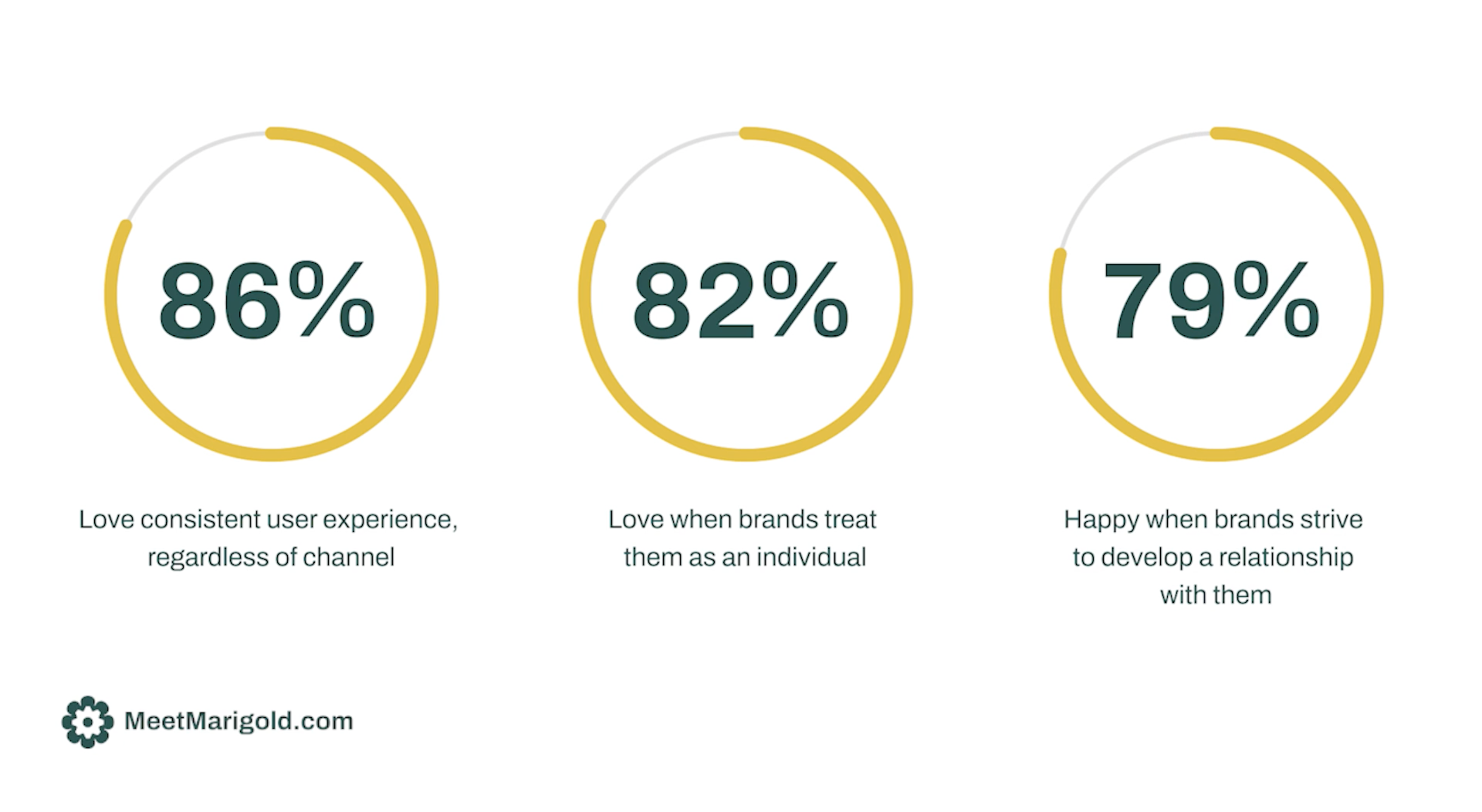

Tim Glomb: Cool. Well, look, let's dig in, all right? I ate up a lot of time kicking this thing off. I propose we kick off with a little discussion around the need for all brands today, especially finserv, to adopt a true relationship marketing strategy. What I mean by that is less marketing at consumers and more interaction, conversation, listening, and frankly, meeting them where they are or where they want to be. After all, people want to be treated as an individual today, and 74% of consumers declared that, and that's a 110% increase from last year per our digital consumer trends index. What I'm referring to is that 2022 digital consumer trends index, which pulled over 5, 000 global consumers in six countries. This is the third year of this report. So, some great year- over- year trends revealed in the 90- page- plus report, which is free to download at consumertrendsindex. com. Justin, that's my kickoff.

Justin Orgel: Thanks, Tim. It's definitely a great stat, and definitely falls in line with what we're seeing and hearing from our current finserv clients. They want to meet those audiences where they are and treat them as individuals, which is paramount. Finserv brands have one of the most accelerated digital transformations in decades, and consumers demand even more personalization along with ease of use. That means financial products themselves need to be easy to use, but also customer service has to be flexible and make their service available on all channels, especially mobile. I also want to call out that traditional financial and insurance institutions are continuously being disrupted by competitors on both these product and experiences levels, and it exposes a huge gap in the market. One of the most well known fintech companies in the past decade, which I think exemplifies this disruption, is SoFi, or short for Social Finance, which I think many of you have probably heard of at this point. Initially, they focused on a digital lending platform for student loans with low interest rates, and then they grew their business very fast, and now they've positioned themselves as the New Age bank for Millennials and Gen Z. They're an important and classic example of a company that's now at a maturity phase that's doing a lot, that has really focused on those two gaps that we'd seen from traditional banks.

Tim Glomb: Look, and not just a New Age bank for Millennials and Gen Z. I'm a Gen Xer, and I have completely changed the way I bank. So, it's great to look at these companies who have completely embraced the shift and change in the landscape, and adopting technology to make their services and products better. It's good, and it's a great call- out. People should definitely go look at them. But look, there's more data from the consumer trends index that supports that initiative: digital transformation, et cetera. And when it comes to loyalty and long- term value for customers, 55% of those consumers said they remain loyal to a brand because their products, and 38% because their customer service is strong. So, when you talk about New Age banking, that's a core competency for them, customer service. Do I have to go into a branch? Can I just use an app? Can I text? Furthermore, 52% declared that they use a mobile phone while they're in a physical store or location to research or help them decide to make a purchase, and a hefty 47% claimed to have browsed for products in a physical store, but purchased online. Just some stats. Go get the consumer trends index. There's a ton of stuff in there. I don't care what industry you're in, but finserv should definitely be looking at that. But let's look at the four stages of relationship marketing. That way we can hone in on the full customer life cycle, and start to shape up where we feel finserv brands really need to focus today. The four stages of relationship marketing are simple, but here they are. First, it's all about acquisition. You have to turn that unknown consumer into a known customer. It's very, very simple, and simply just get them into your database. Maybe that's through a value exchange offering where you give something of value to an unknown consumer, and they provide basic information that you can put onto their record or their file. Or maybe it's their first transaction with you, and they're a new to file record being created. That's really important. That's acquisition. Stage two is enriching that data that you have on that now- known consumer to understand their individual wants and needs. Tim is different from Justin; everybody has different needs. And this is not about buying data on a consumer or an individual to round out their profile, but rather continuing that value exchange in conversation; progressively profiling, chipping away and getting more. Ask them questions via surveys, or even a sweepstakes, or offering discounts and exclusive content, maybe educational resources; all of that in exchange to learn more about their psychological needs. We're going to show this in action in a few minutes when we share that Kiwibank example, but that's the second stage. Stage three, it's all about engagement, baby. This is where you already learned about your customers, what they want, how they want to be communicated to, what frequency, and then you can develop highly personalized messaging across email, mobile, in- app, your websites, all the channels that you own, including advertising. So, creating value in those messages by using individual data at the individual level: that's what people want. And stage four, once you've got the machine running, it's all about loyalty and retention. Keeping that conversation going with your customers, continually refining your offerings at a personal level, and recognizing them for their loyalty and business. That's not just recognizing their transactions; recognizing that they're with your brand, they're on your site, they're coming into your locations, et cetera. That's important. And simply recognizing someone's interaction with your brand is a great way to foster loyalty and retain those customers over the long term. There, now I've defined the four stages of relationship marketing, Justin. I just wanted to get it out there at the top.

Justin Orgel: No, that's great. Good explanation, and this is something that our strategy team regularly collaborates with all clients, especially in this context, finserv. We typically when we work with a client, we'll break out the client goals into categories. The first category is marketer goals: what is the marketer, our client, what are they trying to achieve, and how can Cheetah help them exceed those goals? This can be everything from operational excellence, data integration, ROI measurement, increasing percentage of segmented campaigns, converting a percentage of unknown audience to known, filling in customer gaps, and then banking- specific metrics such as percentage of accounts opened online, is a common metric that we work. That's marketer goals. The second part of this is customer goals, the end customer. What behavior are we trying to drive by leveraging our engagement software? For finserv clients, again, this can be... Common ones include increasing the number of products utilized by existing customers. So, growing loans by X percent, growing deposits by Y percent. Increasing personalization in customer campaigns. This ties back to Tim's point earlier around the customer study and individuality. And finally, thinking more holistically, the digital experience as a whole. This is typically measured by digital adoption. So, our customers using your mobile app, online accounts, and ultimately NPS scores. We're fortunate enough to work with a lot of highly- acclaimed finserv clients that are leaders in customer satisfaction, and one of the fun challenges has been to help them transform and extend this into a digital transformation, into new channels, and really showcase how traditional institutions can also be great stewards of customer service in the digital ecosystem.

Tim Glomb: No, this is great. I love the way you break it down into the marketer's goals and the customer's goals, because you've got to keep that customer- obsessed, customer- focused attitude. And to your point, when you talk about are they engaged in the adoption, those KPIs, are they using your app, are they using the online accounts, those are all signals. Those are all signals and opportunities to reengage somebody. I love it, and the customer engagement platform that we've built can ingest all those. For retail, it's bringing in point of sale; for travel, it's bringing in weather data. You can bring in an unlimited amount of batch or streaming data in our platform and listen to these signals, and web app or mobile behavior is one of those. Love it, love the way you guys attack that. But I want to share this Kiwibank example, because I think it really does tackle the first three stages of relationship marketing really, really well, and they had incredible results using the customer engagement platform to execute this. Just to set it up, the goal for Kiwibank was to go to market with a value offering that would tell the consumer exactly what kind of money personality they had, and then match their products and services to the individual, along with resources and information that could be explored by the consumer on their own. So, really an educational play and a brand awareness play, but really giving them some personalized content. They promoted this campaign in all the channels you'd expect. They went to social, they pinged their existing contacts and email databases. I believe they even promoted it in locations with maybe QR codes or texting to engage. So, the promotion; pretty standard stuff. The first stage here was an acquisition play using Cheetah Experiences, which on the front end of the customer engagement platform really is our gathering tool. It gathers that rich zero- party data directly from an audience. They developed a very simple survey that tracked answers from each recipient related to their spending and saving styles, along with their outlook for the future, and even some questions regarding their mood and situations that caused them to either spend or save. I really like the way they set up the acquisition piece here.

Justin Orgel: This survey was clearly strategic, and every question was created to add value to the brand and their future communications, so they could get a better sense of the individual, and then mapping all of that data into our platform to execute across the three stages of relationship marketing strategy with inaudible. Another note I thought would be important to mention here is just the importance of just continually collecting and refreshing customer profiles. The pandemic was really an interesting learning I think for a lot of clients and just brands in the sector, because it allowed companies to reevaluate their target audiences, intentions, accelerants, and the financial demands in the early stages, and then where we're at now at the more mature stages of the pandemic. I wanted to just share a client example, and thinking about static data versus active data, when you think about your universe and your customer profiles. If you think about pre- pandemic traditional banking, you'd have segments, would be you have your unknown prospects, you have maybe your mortgage prospects, maybe your retail bank and credit cards, maybe your business- to- business treasury services. If you think about the post- pandemic, not just the people that are your customers, but also the products that you service, thinking about refinance revolution. All of these, the low interest rates spur a huge refi revolution. How do you target the people that might be eligible? Not just prospect audience, but people that are actually looking to refinance. The other thing was around business PPP loans, government loans, and how you can target your business prospects or customers for these type of loans. Another one I call HELOC heroes, home equity line of credit. The value of people's homes were increasing significantly. People wanted to pull money out of the value of their homes. How do you target those homeowners who are opportunistic and want to take advantage of that? And then also these branchless digital banking natives. If you think about the fintech world, there's a lot of different banks that are being created and they're branchless, there's no physical locations. How do target the people that are not necessarily tied to a brick and mortar experience?

Tim Glomb: Man, I knew we brought you to this webinar for a reason. That's great insight on the finserv. And I'm part of that, I was part of the refi revolution, and digital branchless banking, my kids use Greenlight. One is a teenager, one is sub- teenager, they probably never will know what the experience of an in- store banking is, like when you and I grew up. Remember going and getting some money from your grandma from your birthday and putting it in the bank?

Justin Orgel: inaudible

Tim Glomb: Those days are changing. Well, look, and kudos to you guys, because what we're looking at here on the Kiwibank example, which I want to continue, is strategic services really guided that. If you're watching this right now going," Oh geez, strategic surveys and the questions. What would we ask? What can we activate?" That's why we have strategic services. They know your business, they know your industry, so they can figure out what are the strategic data points you need to get from your target audience to then be able to inform your products and services. I want to continue with that, because once Kiwibank's strategic questions were mapped, which we just showed, now an individual submits that form and they get an instant gratification, which is so important in today's age, especially if we're talking about targeting Gen Z and Millennials. In this experience, they were told exactly what kind of saver or spender they are, which was determined from a handful of different outcomes. Based on their answers, we had some preset outcomes. Here's where the engagement stage, stage three of relationship marketing, really comes in. Each consumer was now set on a journey filled with emails and SMS messages over the next few months that were serving up amazing content tailored exactly to their individual needs. Here's what my journey looked like. I actually have the email. They identified me as a security saver; I guess I'm proud to say I passed the test. My first email, it fired off immediately after I hit that submit button on the value exchange survey, and it was loaded with videos, article links and podcasts that would help me identify better spending and saving habits along with Kiwibank's products and services to help meet my goals. So, from get- go, literally within seconds of submission, I automatically had these resources. I love the way you guys set this up, it was really slick, and kudos to you guys, because the instant gratification is what gets those open rates and those engagements up. So, kudos to you.

Justin Orgel: I think foundationally it's just a great value exchange. It's far better to ask a few questions from your engaged audience and serve up custom and personalized content that meets their declared needs, rather than take a passive approach and just let the consumer visit your website on their own, digging and searching for what they think they might need. This is why retail stores have people on the floor, to help them find the product they need by asking a few questions. So, great execution in the digital world here. Second, the content was curated individually, and it was dynamic, delivered immediately after they submitted it. Real- time engagement really does have a conversational tone to it. Waiting to send an email and SMS after someone took action with your brand is the kiss of death. Consumers expect real- time, and engagement rates show this is worth the investment. We see this over and over. If you can get a response immediately... We have a lot of stats and data to support that real- time interactions drive more engagement overall. Over 50% open rates on email when it's done in a real- time manner, and some of the highest engagement rates with that personalized content, meaning they're engaged, ready for the next step in the conversation or the relationship.

Tim Glomb: And it's relationship. Well, some people who weren't in the Kiwibank fold, they were new to it because of the promotion and the survey and the value exchange, they're now building a relationship, which is exactly what you need to be doing as a brand. So, great, great stuff there. But there's also some stats that back all this up. Let's use some data to empower what we're actually trying to convey here. The number- one most annoying gripe consumers declared in the consumer trends index this year related to messaging, and I'll call messaging email, SMS and in- app message or personalized messages on a website when you're visiting, is that they were getting irrelevant content and offers. You mentioned before, ask a few questions, keep the conversation on track; 49% of those consumers declared that irrelevant in content and offers was what was driving them crazy. That's a fact that you can use to map your content and offers directly to an individual, and when you do it's incredibly powerful. I'm sure most marketers watching right now are still casting and blasting generic, one- size- fits- all messages to their audiences, or at best you're guessing which content some segment: male, female, high income, low income, what they might want. You're guessing, and marketers shouldn't be choosing for their audiences any longer. Those days are gone. You need to ask questions, and you need to match your response to that. If I asked you, Justin," Hey, do you love spaghetti?" and you said no, and I said," Come on over for a spaghetti dinner," you'd look at me sideways, like I didn't listen. That's totally true, especially for a finserv brand, in my opinion, where the shift from an on- site legacy over- the- counter transaction, that desk, it's shifting to what you mentioned, these headless and digital banks. Today, sales and customer service, it all happens in chat rooms, it happens on mobile phones. As our Star Wars hero Mandalorian would say," This is the way." It's got to be digital.

Justin Orgel: Exactly. What does that say about the preferred messaging channel? We provide a ton of email and mobile messaging along with wallet and in-app messaging for thousands of clients. But what does the most recent data suggest as far as the channels consumers prefer?

Tim Glomb: That's a great question, because you do have to factor in what channels are working, and I'm intimately familiar with this. Consumer trends, this is our third year now, and I've been eating this thing, I've been living it nonstop for the past few months. So, here you go. First and foremost, email is still the reigning champ for messaging and engagement in an owned channel, something you can control; no algorithm in the way, no paid media or anything like that. In fact, email was the number- one preferred channel, over paid ads, over SMS, over organic social posts and bare ads. So, in general, email is the one. In fact, even the Gen Z audience saw 43% of them purchasing from the email channel, with 63% being the strongest from the group, which was the Boomers. We get it: boomers, they still love email, but Gen Z, they're still using it. So, email is alive and well, there's no doubt about it. It's beating the other channels. It's one of the easiest channels, by the way, to personalize. You can literally map dynamic content in emails to any given data field from any given individual that you have on record, and you can bypass all those segments and lumps and cohorts. You can literally treat people as an individual, and take data from their profile and go right to the source. So, serving content based on data they provided, what can get more personal than that? By the way, we toss out a lot of stats and trends like this, but I think it's worth noting another research firm confirmed that email is the number- one preferred channel from consumers as reported in eMarketer's Insider Intelligence this spring. Here's a chart. Multiple research firms are confirming the strength and relevance of email as a channel. So, if you do not master email, you're in trouble. Here are some other stats that aren't ours. But anyway, let's look at mobile too, specifically SMS and MMS, as drivers of purchase. I was really surprised at these figures, honestly. They felt a bit low, but here's what the data says. When asked if they made a purchase directly from an SMS or MMS message received from a brand directly, only 18% of Gen Z made a purchase directly from that SMS or MMS message. I would have thought that would have been way higher. 32% of Millennials did so, and 32% of Gen X did, and we saw Boomers drop back down, 17% making a purchase from the SMS- MMS channel. But overall, there was a 19% increase year over year across all age groups making a purchase from email on their mobile device. So, mobile device is solid. It's the channels where the difference really becomes a factor.

Justin Orgel: Really strong numbers there. It goes back to your point about personalization scale, zero- party data informing not only the type of content and offering inaudible, but how easy it is to serve up that content at scale with dynamic formatting so that your message actually resonates. So, no longer is a cool future wish for brands to be able to execute at that level; it's something that's actually happening now. It's alive and well.

Tim Glomb: Look, and you guys do a great job of this. You get new clients, you teach them the way. You do it for them at first, and then they become self- sufficient. I think that's great. And look, personalization, when we talk about email channel, it starts at the subject line. In the Kiwibank example, my subject line in my email was customized to remind me I was a security saver. That was the key word I got instantaneously in the survey, and whenever I got to my inbox, it was there. It reminded me. That piques your interest and gets you into that content. It gets people to open all day long when you bring that relevance to the subject line.

Justin Orgel: Definitely, and one other thing to consider too, with Cheetah we have obviously hundreds of finserv clients on our platform, and a big focus is around security. Not only are we certified real CDP from the CDP Institute, meaning you don't need a slew of vendors to act as your CDP email provider, mobile provider, loyalty provider, et cetera; we do that all in one platform. So, the data flow is seamless, and marketers can actually acquire, view, activate and analyze the data in one platform, and again, working with some of the largest banks in the world. So, that's definitely a big strength of ours and something we don't take for granted.

Tim Glomb: Totally, man. That's super important. Being a former marketer myself, I remember the days of keeping my tech stack working. Sometimes it felt like it was swaying in the wind of a tornado, and communicating, all those vendors communicating with each other, it was a nightmare. I signed 33 SaaS agreements the year before I joined Cheetah as a brand marketer, and that was a nightmare. What I love is our platform approach. It saves you so much time, energy, resources, et cetera, to be able to acquire, engage, send your email, your MMS, see everything in one dashboard, and then even have a loyalty offering. So, I agree with you. It's important to use the power of platform.

Justin Orgel: Totally. Or SOC2 compliance, certified high trust. Many watching right now will know that these are critical attributes when you're talking to a technology vendor, but we really I think have a good blend when it comes to the data privacy and security all combined.

Tim Glomb: Oh, yeah. Can't leave that out, especially in the finserv. You know that far better than I do. It's great to hear all those things we're putting resources and dollars into for security. But I'm going to one- up you a little bit, because I'm not sure if this trumps our amazing security and data practices, but did you know that Forrester named Cheetah Digital a strong performer in the Forrester Wave email marketing services providers, Q1 2022. I'm contractually obligated to say that entire, ridiculously long report title, maybe one day they'll change them. But regardless of the name, it's an industry staple, that report, and it's used to inform many organizations when acquiring new technology, and I'm proud to say that Cheetah Digital earned the highest current offering category score out of all the vendors. This Wave report, it evaluated I think 13 significant providers of email; Acoustic, Adobe, Oracle, Salesforce, Zeta, all of them. So, I got to get the shameless plug in there. And the quote that they put, which was this report goes on to suggest that," Big retailers, banks, and hotel chains that want comprehensive relationship marketing, not just email or mobile messaging execution, will find Cheetah Digital's white- glove service unmatched." So, not only do we do email well, but we deliver solutions across the entire customer life cycle incredibly well. But don't take our word for it. Go get that Forester Wave email marketing service providers Q1 2022 report from our website right after the session. It's going to be on the same page, and get it here. Look, if you're IT- focused, you're going to enjoy that report because it has a ton of tactician and marketing- level stuff. I just think you're going to love it. And kudos to you, Justin, and that white- glove service that we were touted for.

Justin Orgel: Yes, I have my gloves on inaudible.

Tim Glomb: It's all white- glove. Well, look, we're almost 30 minutes into this thing. I think we did a pretty good job today exploring the first half of a relationship marketing theory. Acquisition, understanding people, we showed the Kiwibank. We gave some great stats that support this strategy. Zero- party data, acquiring new context, enriching the data, all that. I think your insights from the strategic services team here at Cheetah Digital is a huge benefit to this audience as well. So, I'm proposing we do this again. We come with maybe some other examples, maybe a client, and look at the other side, the loyalty and retention side of marketing efforts, the next time we do this. What do you think?

Justin Orgel: Yeah, that sounds great. Look forward to it.

Tim Glomb: Cool, cool, cool. All right, well, again, we appreciate you watching. You've got a ton of resources here right on this webpage where you're watching. You can always go to the resources section at cheetahdigital. com. You can always smash that" book a meeting" button. We're happy to talk to you. We'll get someone like Justin on the phone with you and assess your needs. We do a ton of content. Come back, see us, subscribe to Thinking Caps podcast on Apple or on our LinkedIn page, and we'll see you in the next event. Adios.

DESCRIPTION

Finserv industries have seen some of the biggest digital transformations in recent years and consumer demands have changed the way they operate. Stats show that you need to adopt a customer obsessed relationship marketing strategy to survive. And you most likely need to change your entire customer experience.

In this session we’ll explain the 4 stages of relationship marketing from acquiring new customers, understanding them as individuals, engaging them across all channels and ultimately retaining their business and fostering loyalty. We’ll show how Kiwibank is getting this process right and learning more about their target audience while engaging them, in real-time, to bring them closer to their products and offerings.

Also hear from the Cheetah Digital Strategic Services team who reveals some of the common solutions our clients are using to drive their business forward. Understand what your peers are doing and what strategies and tactics can be implemented in your organization.

This is part 1 of a 2 part series to help finserv organizations level up their customer experience and usher in a new way of doing business.

Today's Guests

Justin Orgel

Tim Glomb

Recent Episodes

The 2023 Global Consumer Trends Index Webinar

Episode 130 | 02.28.2023

The Value of Zero-Party Data and How Brands Large and Small Are Activating It

Episode 129 | 02.27.2023

The 2023 Global Consumer Trends Index Webinar

Episode 128 | 02.24.2023

How is Relationship Marketing the key to converting consumers into advocates?

Episode 127 | 12.14.2022

Experts Tell All: How Industry Giants Use Data to Speak Authentically to Diverse Audiences

Episode 126 | 10.27.2022

The Sweet Personalization Strategy That Gives Magnolia Bakery a Greater Customer Return Rate

Episode 125 | 10.27.2022